Describing the EBA’s position in regards to the supervision of the Fintech industry, the chairman of the EBA, Andrea Enria, said regulators need to maintain a “measured approach”. Next week the EBA will publish it’s roadmap defining it’s regulatory priorities over the next two years.

The head of EBA was speaking at the Copenhagen Business School on Friday, where he said that cryptocurrencies should not be placed under the regulations that apply to the traditional financial system. Several central banks have argued that cryptocurrencies lack the institutional backup and cannot fulfil the functions of money – unit of account, means of exchange and reserve of value.

Andrea Enria said:

“Still, I am yet to be convinced that this is sufficiently strong argument to attract cryptocurrencies under the full scope of regulation”

Enria remarked that the policy debate on technological and financial innovation often focuses on two opposite approaches: “regulate and restrict” – banning innovative business not fitting into the rulebook; and “let things happen” – rooted in the belief that a dynamic financial sector needs breathing space to innovate. In his opinion, both regulatory strategies have shown their limitations, with the first being ineffective in open markets, and the second one increasing risks in the unregulated sector.

Andrea Enria on #Fintech Copenhagen Business School. Click here to read the full speech: https://t.co/JNwB3bx8Z2 pic.twitter.com/fqyzgVzL0i

— EBA News (@EBA_News) March 9, 2018

The EBA outlined a framework for regulation of crypto in 2014, noting that its development would require many years and a nuanced strategy. Its approach was focused on warning consumers that their crypto investments are not protected, and preventing regulated financial institutions from buying, holding or selling cryptocurrencies. EBA had also proposed segregating banks and crypto operators, in order to avoid what they called “contagion”.

Enria thinks certain functions, such as providing liquidity in crisis situations and lending, should be strictly reserved for the banks and subject to “enhanced regulation and supervision”. At the same time, services, like payments and issuance of electronic money, may be provided by other intermediaries. These services are not intrinsically related to the essential functions of banks, the head of Europe’s banking authority argued.

The crypto sector is changing fast and it’s difficult to regulate and supervise, Enria admitted. Authorities have to continuously review regulations, but they also need to maintain an informed and measured approach, he added. Small innovative startups cannot sustain the compliance burden placed on banks.

Enria warned and stressed:

“An excessive extension of the regulatory perimeter, attracting most Fintech firms under the scope of bank-like supervision, just because they compete with banks in some market segment, is likely to be a sub-optimal solution”.

EBA’s Chairman is convinced that such move would create the risk of “constraining financial innovation”. He advocates a “proportionate” and “less intense” approach in comparison to regulations applied to the banks, citing “lower potential for systemic risk” from the crypto sector.

In these areas of business, we may well let innovators experiment with new products and business practices.

The Chairman of EBA said, however, that regulators should never allow de facto banks to combine deposit-taking and lending outside strict regulatory requirements and effective supervision. Any financial firm doing that should be regulated and supervised as a bank.

The first step for regulators should be to understand how new products and business practices fit in the existing regulatory framework, Andrea Enria said. The conscious choice not to impose the full set of rules on a nascent technology can lead to a more mature and productive dialogue between innovative firms and regulators, he added.

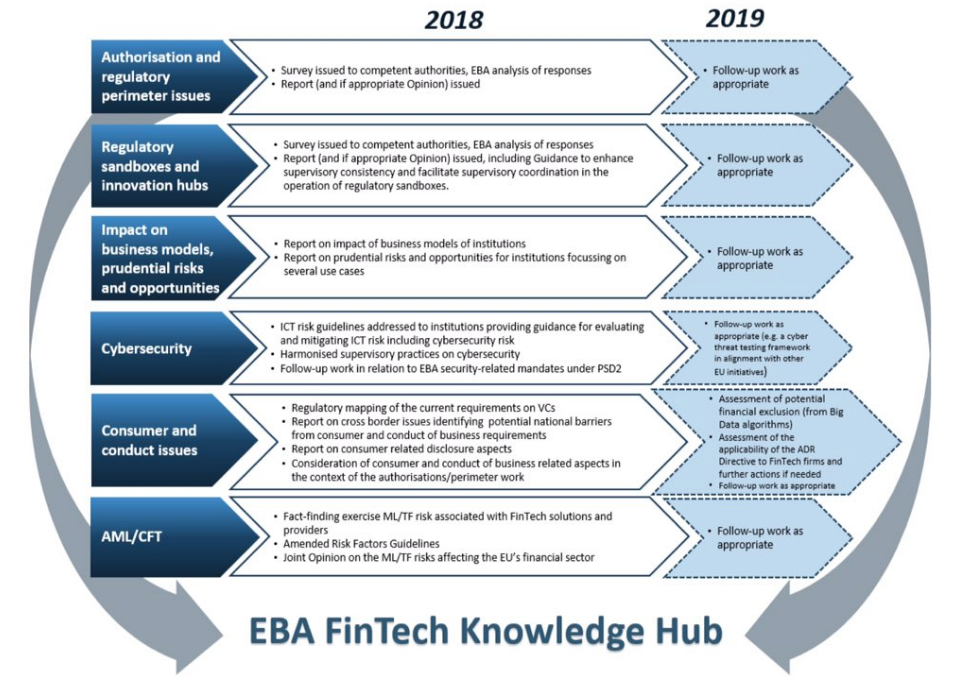

According to EBA’s executive, the debate on how to regulate innovation is often “laden with prejudices and undue simplifications”. In his view a “proportionate, technologically neutral approach” to regulation should be pursued, while avoiding “inherent bias towards the status quo”. This can be achieved through monitoring the existing regulations and setting up sandboxes to facilitate consistent rules to support new technologies and innovative business models. To ensure that supervisors understand these new technologies, EBA intends to create a “knowledge hub” and introduce technological neutrality into supervisory guidelines.

Andrea Enria supported calls for consistent approaches towards regulation across Europe’s Single Market. That would guarantee entities across the Union receive equal treatment and opportunities.

EBA’s chairman said:

“Fintech firms must be able to scale up and offer services across the Single Market, providing benefits to all EU citizens”

He also noted that competition in the Fintech space is developing globally and warned European businesses would have to cope with significant disadvantages, if local authorities impose different sets of rules. Current variations may result in “regulatory arbitrage” or consumer protection risks.

The European Commission has recently issued a Fintech Action Plan with several mandates for the European Banking Authority. Next week EBA will publish its “Roadmap on Fintech” defining a series of regulatory and supervisory priorities for the next two years. EBA wants to analyze provided services and their regulation to ensure consistency across the EU. The banking authority expects to report on its assessment before the end of 2018.

EBA will also conduct further analysis of implemented sandbox regimes to identify best practices and develop guidelines. The EU body will review approaches to licensing in member-states and may recommend amendments to the European financial services legislation. According to Andrea Enria, EBA will try to identify potential national barriers and consider steps to remove them, in order to allow scaling up of innovations.

Overall the speech was positive for the developing crypto sector in Europe and should provide some clarity for investors.

Comments are off this post!